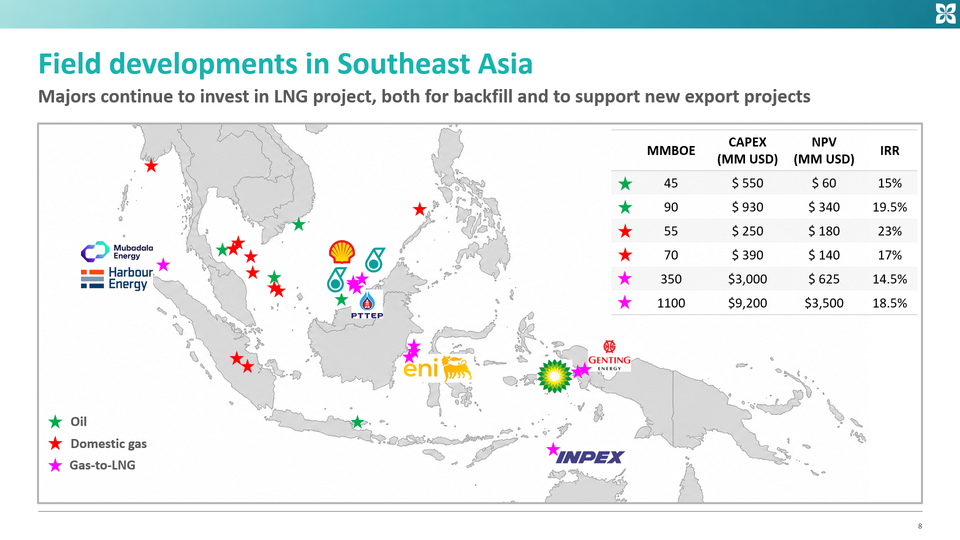

Domestic gas developments in Southeast Asia

Kawi Energy presented at the SEAPEX / GESGB event in London on June 17th 2026. We were asked to talk about field developments in Southeast Asia.

We have split the presentation across a number of videos, with each video looking at a different resource class. In this second video, we look at a selection of domestic gas projects, and what they tell us about the above-ground factors that can enable, or delay, development.

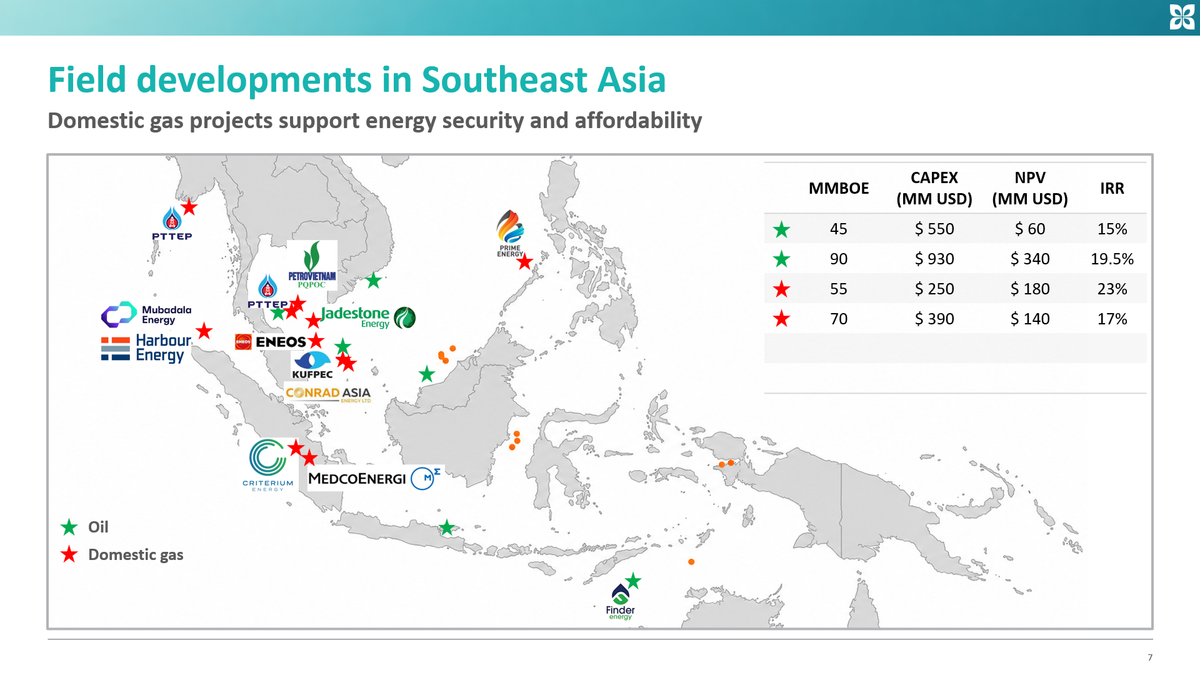

Domestic gas is arguably the most important upstream theme in Southeast Asia from an energy-security perspective. These projects support power generation, industrial demand and affordability, while also helping governments manage reliance on imported LNG or declining legacy supply.

However, domestic gas is rarely straightforward. Projects can be held back by access to infrastructure, gas sales agreements and pricing, carbon management, development sequencing, partner challenges and wider political considerations. The strongest projects are therefore not just those with the largest resources, but those where the subsurface, infrastructure, buyer and policy environment all line up.

Indonesia - Criterium - SE-MGH

At the smaller end of Southeast Asia’s gas development pipeline sits Criterium’s Tungkal PSC in South Sumatra.

Criterium completed its acquisition of Mont D’Or Petroleum in 2024, acquiring two operated assets in the Tungkal and West Salawati PSCs. The Southeast Mengoepeh, or SE-MGH, project will develop gas resources in the Tungkal PSC, with a low-cost scheme utilising existing wells and processing facilities. The project is expected onstream in the third quarter of 2026.

The target initial production rate is around 5 to 8 million cubic feet per day, with gas sold into the domestic market under a long-term take-or-pay contract. Criterium has indicated that pricing is expected to be fixed, or broadly aligned with recent South Sumatra gas sales of around US$6–7/MMBtu, giving the project a relatively predictable cash-flow profile once the binding gas sales agreement is finalised.

The prize is not large by regional standards, but it could be transformational for Criterium. SE-MGH would provide near-term cash flow, help the company pay down debt, and give it a platform to look at further development and acquisition opportunities in Indonesia.

Indonesia - Medco Energi - Kaliberau Dalam

Nearby in South Sumatra, we have Kaliberau Dalam.

The field was discovered by Repsol in 2019 to much fanfare. It was promoted as Indonesia’s largest gas find in years, with early talk of at least 2 Tcf of recoverable gas. However, that scale has not materialised. After appraisal, the current development case has been resized to around 474 Bcf, with earlier POD guidance pointing to around 288 Bcf of sales gas. The gas also contains around 26% CO₂, adding a carbon-management challenge to the development.

Medco has become a key producer in South Sumatra, strengthening its position through a series of acquisitions. It acquired ConocoPhillips’ stake in the Corridor PSC in 2021, then agreed in 2025 to acquire Repsol’s 24% stake in Corridor, lifting its interest in the mature gas hub to 70%. Medco then moved on Sakakemang itself, agreeing to acquire Repsol’s operated 45% interest in the block, along with an 80% interest in South Sakakemang.

Repsol had already brought Kaliberau Dalam to POD approval, but Medco now has the opportunity to optimise development around its wider South Sumatra position. The field can be integrated with the Corridor hub, using existing facilities, long-term buyers and Medco’s market access to do much of the heavy lifting.

The complications remain. Kaliberau Dalam is high-CO₂, the project has been resized from its original hype, and commercial execution still matters. But under Medco, it looks less like a stranded Repsol discovery and more like the next bolt-on molecule for Indonesia’s South Sumatra gas machine.

Indonesia - Conrad - Mako

Moving offshore, Conrad’s Mako project in the West Natuna Sea is a classic case of gas monetisation being harder than discovery.

The field itself was never the problem. Mako is a shallow-water, fully appraised gas resource, close to the West Natuna Transportation System — infrastructure that has been moving Indonesian gas to regional markets for decades.

For years, that seemed to make Singapore the obvious destination. Conrad advanced gas sales terms with Sembcorp, and the project was framed around exports into a premium, established power market.

But the politics of gas allocation intervened. Indonesia has become more focused on domestic energy security, and the Singapore sales route ran into regulatory resistance. In 2025, Sembcorp terminated its import agreement after the required Indonesian approvals failed to come through.

That could have stalled Mako. Instead, it forced a reset.

The project has now been reworked around Indonesian domestic offtake, with gas moving through Kakap and the WNTS system before delivery into PLN-linked infrastructure for the domestic market. That shift helped unlock final investment decision in March 2026.

There is also an M&A and funding angle. Conrad’s farm-down of a majority Duyung interest to Nations Natuna Barat brings in an Indonesian partner to fund development and carry the project through execution. That matters because the political destination of the gas and the ownership structure now point in the same direction.

The development is now tangible: six wells, a leased MOPU, a 59-kilometre pipeline connection, and more than US$280 million of contracts awarded. First gas is targeted for the fourth quarter of 2027.

Indonesia - KUFPEC - Anambas

Also in the West Natuna Sea is KUFPEC’s Anambas project — a development that has moved forward, but has not yet fully crossed the line.

The Indonesian government approved the POD in 2025, giving KUFPEC a formal route to develop the field. On paper, this is a meaningful offshore gas-condensate project: around 55 million cubic feet per day of gas, roughly 185 billion cubic feet of total gas sales, and an investment number of about US$1.5 billion.

But unlike Conrad’s Mako, Anambas has not yet reached final investment decision.

That makes the story more provisional. The enabler is clear: Anambas can use existing West Natuna gas infrastructure, including subsea pipeline links into the West Natuna Transportation System. That gives the project optionality into domestic and regional markets, and fits Indonesia’s push to lift domestic gas supply while keeping existing export systems utilised.

KUFPEC also has strategic reasons to push it forward. Anambas would deepen its Natuna Sea position, building on its stake in Natuna Sea Block A, and sits within a broader Indonesian expansion push that includes new exploration acreage and interest in larger regional gas opportunities.

But the hurdle is commercial commitment. POD approval shows government alignment; tendering shows preparation. FID will show whether gas sales, pricing, infrastructure access and project economics are robust enough to justify the spend.

Malaysia - PETRONAS / ENEOS - BIGST

Moving into Malaysia, the BIGST cluster is one of the clearest examples of the next generation of Southeast Asian gas development.

The resource is not new. BIGST — Bujang, Inas, Guling, Sepat and Tujoh — was discovered decades ago offshore Peninsular Malaysia, but remained undeveloped because the fields contain high levels of CO₂.

That makes BIGST less a conventional gas project and more a test of whether Malaysia can commercialise high-contaminant gas at scale.

The prize is important. Peninsular Malaysia needs new domestic gas supply, and BIGST has the potential to become a material source of molecules close to the market. But unlike lower-CO₂ tie-backs, it cannot move forward simply by connecting wells to existing infrastructure. The CO₂ solution is central to the development.

That is why PETRONAS brought in ENEOS Xplora, formerly JX Nippon, on a 50:50 basis. This is not M&A in the classic sense; it is partner selection as an above-ground unlock. ENEOS had already been studying low-emission development concepts with JOGMEC, and the BIGST plan is built around separating, capturing and injecting the CO₂ produced with the gas.

The project has moved forward: the PSC was signed in 2024, FEED entry was endorsed in 2025, and PETRONAS and ENEOS are targeting FID in 2027.

But the gating issue remains carbon management. BIGST could unlock a new high-CO₂ gas hub for Peninsular Malaysia. Or, if the CCS chain proves too costly or complex, it could remain another example of gas that is technically discovered but commercially stranded.

Vietnam - Jadestone - Nam Du / U Minh

Moving into Vietnam, Jadestone’s Nam Du and U Minh project is a story of a long-stranded gas resource finally becoming developable.

The fields sit offshore southwest Vietnam, close to infrastructure that already feeds the Ca Mau power and industrial complex. That location matters. Production from the PM-03-CAA block is declining, creating available capacity in the pipeline system that Jadestone can use for new domestic gas.

For years, the missing pieces were not really subsurface. They were government approval, gas sales terms and a development structure that could justify final investment decision.

In 2026, two of those pieces fell into place. First, the Vietnamese government approved the field development plan for Nam Du and U Minh, allowing Jadestone to book initial 2P reserves of 32 million barrels of oil equivalent. Then Jadestone signed a full gas sales and purchase agreement with PV Gas, the gas arm of PetroVietnam.

The project now has an approved development concept, an offtaker and a route to market. The plan is to develop the fields with two unmanned wellhead platforms, process production through an FPSO at Nam Du, and export gas through PetroVietnam’s existing pipeline to Ca Mau.

But Jadestone has not yet taken FID. Instead, the company is using this year’s progress to launch a farm-out process, aiming to bring in a development partner before sanctioning the project. Here, M&A is the next catalyst rather than the past catalyst: the approvals and GSA make the asset easier to partner because a buyer is no longer taking pure stranded-gas risk.

The approvals and GSA have de-risked the story; the next test is whether Jadestone can bring in the right partner and funding structure to carry it through FID and toward first gas in late 2028.

Vietnam - PVEP - Block B

Also in Vietnam, Block B is the country’s flagship gas-to-power project — and a reminder that FID does not always mean fast execution.

After years of delay, the Block B–O Mon chain finally reached final investment decision in 2024. This was a major breakthrough. The upstream project is large, with plateau production expected at around 490 million cubic feet per day, while the full chain — field development, pipeline and downstream power plants — represents one of Vietnam’s biggest domestic gas investments.

But Block B is not just an offshore gas project. It is a gas-to-power system. The gas only has full value if the pipeline and onshore power plants are ready to take it.

That is where progress has again looked uneven. The upstream and midstream pieces are moving: EPC work has been awarded, pipeline fabrication is underway, and Petrovietnam has secured major financing for the field and pipeline. But the downstream side is still catching up. O Mon IV only broke ground in 2025, with commercial operation targeted for late 2028, while O Mon II has faced delays linked to project guarantees, gas and power contracts, and financing.

This is the core above-ground issue. Block B has the reserves, the partners and now the FID. What it needs is synchronisation across the whole chain.

For Vietnam, the prize is significant: domestic gas supply, reduced reliance on imported LNG, and new baseload power for the Mekong Delta. But if the power plants lag, the upstream project cannot ramp as planned.

So Block B is not stalled in the old sense. It is sanctioned, partly financed and under construction. But it remains vulnerable to the weakest link in the chain — the downstream power build-out.

Thailand - PTTEP - Bussabong

In Thailand, PTTEP’s Bussabong discovery shows why infrastructure ownership can turn a modest gas find into a fast-cycle development.

Bussabong sits immediately west of the Bongkot field, one of Thailand’s core Gulf of Thailand gas hubs. That location is the story. This is not a remote discovery waiting for a standalone development concept. It is a near-field accumulation next to a system PTTEP already operates, with existing processing capacity, established gas marketing channels and a domestic buyer base that needs supply.

The timing also matters. Thailand’s mature Gulf of Thailand fields are under pressure, and PTTEP is under a national energy-security mandate to maximise domestic production. That gives Bussabong a clear policy tailwind.

The project has moved quickly. PTTEP drilled an exploration well that encountered gas pay, the area has been identified as a prime candidate for fast-track development, and the Department of Mineral Fuels approved the Bussabong production area designation in early 2026. Final investment decision could follow this year, with first gas targeted around 2028.

There is also an M&A angle. Valeura has farmed into PTTEP’s Gulf of Thailand exploration acreage, giving it exposure to Bussabong and potentially its first Thai gas reserves, while PTTEP remains the natural operator and infrastructure owner. The balance is important: Valeura gets exposure to gas upside, but the fast-track logic depends on PTTEP’s Bongkot hub.

Philippines - Prime Energy - Malampaya

In the Philippines, the gas story is once again centred on Malampaya.

For more than two decades, Malampaya has been the country’s only indigenous source of natural gas, supplying power plants in Luzon and reducing dependence on imported fuels. But the field has been declining, and without new investment it was heading toward depletion.

That is why Prime Energy’s Phase 4 programme matters.

There is a major ownership story behind it. Malampaya has moved from international-major stewardship into a Philippine infrastructure-led platform under Prime Energy and Prime Infra. That matters because the new owner has a direct strategic incentive to extend the life of the asset and keep indigenous gas flowing into the Luzon power system.

The company is drilling and tying back new subsea wells around the existing Malampaya infrastructure, including Malampaya East and Camago, while also testing nearby exploration potential. In early 2026, the Malampaya East-1 well delivered the Philippines’ first natural gas discovery in more than a decade, with gas and condensate found just five kilometres from the existing field.

This is not a greenfield project. It is a life-extension strategy. The above-ground enabler was the 15-year extension of Service Contract 38, which gave Prime Energy and its partners the licence duration needed to justify new drilling. Once that was secured, the consortium could move quickly: drilling, subsea installation and pipelaying are now underway, with first gas from Phase 4 targeted for the fourth quarter of 2026.

The political backdrop is also supportive. The Philippines wants more domestic gas, less coal dependence and less exposure to imported LNG. Malampaya Phase 4 helps on all three fronts.

But the scale should be kept in perspective. These wells will squeeze more domestic gas out of the country’s only proven gas hub, while the wider Philippine gas market increasingly relies on LNG imports.

Myanmar - PTTEP - M-3

Moving to Myanmar, PTTEP is moving forward with the M-3 development, centred on the Aung Sinkha gas fields.

This is a very different above-ground story from Malaysia, Vietnam or Thailand. The market logic is clear: Thailand needs gas, Myanmar’s existing export fields are declining, and PTTEP already has deep operating experience in the country through Yadana and Zawtika.

That gives M-3 a strong strategic rationale as a part of Thailand’s wider effort to protect regional gas supply and reduce exposure to LNG imports, while also sustaining Myanmar’s role as a pipeline gas supplier.

After years on the backburner, PTTEP appears to have taken final investment decision in 2026, with first gas potentially around 2028.

Indonesia - Mubadala - South Andaman

Most of the projects so far are about domestic gas monetisation: smaller fields, tie-backs, existing pipelines, power plants and gas sales agreements. The question is whether discovered gas can reach local markets quickly enough, and at a price that works.

Mubadala’s Layaran and Tangkulo discoveries are different.

Here, the issue is whether Indonesia has opened a new gas province at a scale that could support a much larger monetisation model. Layaran-1 was announced in December 2023 with potential for more than 6 Tcf of gas-in-place, followed by Tangkulo-1 in May 2024 with potential for more than 2 Tcf of gas-in-place. Together, they have turned South Andaman from an exploration concept into one of Southeast Asia’s most important new gas plays.

That changes the conversation from tie-back economics to basin development. Indonesia will want the gas to support domestic energy security, especially power and industry in Sumatra. But commercially, large offshore gas needs scale, infrastructure and long-term demand. That is where the line between domestic gas and LNG begins to blur.

However, size brings complexity as well as opportunity. A discovery of this scale is unlikely to be developed purely around the fastest route to market. National and regional governments will want domestic gas, onshore facilities, local jobs and wider industrial benefits. Those objectives may improve the project’s strategic value, but they can also slow commercial decision-making.

There is also an ownership angle. Mubadala operates South Andaman, while Harbour Energy’s minority interest is openly in play as part of a sale process. Regardless of how that concludes, Mubadala may ultimately look to bring in a proven LNG operator or LNG portfolio player if South Andaman evolves into a basin-scale monetisation project.

Conclusions

The common thread across these projects is that domestic gas is not short of demand. Southeast Asia needs gas for power, industry, affordability and energy security. The harder question is whether each project can align the pieces needed to turn discovered gas into delivered gas.

The resource is only one part of the equation. Projects also need infrastructure access, gas sales agreements, pricing support, regulatory approvals, financing, carbon management and, in some cases, power plants that are ready to take the gas. When those pieces line up, projects can move quickly. When one piece is missing, even strategic resources can remain stranded for years.

The strongest opportunities are therefore not always the largest fields. They are the projects where the reservoir, market, infrastructure and politics all point in the same direction. SE-MGH, Mako, Nam Du / U Minh and Bussabong show how smaller or mid-sized discoveries can become investable when there is a clear route to domestic demand. Block B, BIGST, M-3 and South Andaman show the other side of the story: larger or more strategic gas projects can offer greater rewards, but they also bring more moving parts.

That is the core tension in Southeast Asian gas. Domestic gas is essential, but it is not simple. It can reduce import dependence, support power systems and create local economic benefits, but it also requires coordination across the whole value chain.

South Andaman points toward the next question. At a certain scale, domestic gas and LNG stop being separate stories. Large resources may need domestic markets, industrial demand, export optionality and LNG-linked partners to make the development work. That is where the next part of the story begins: Southeast Asia’s gas-to-LNG projects.