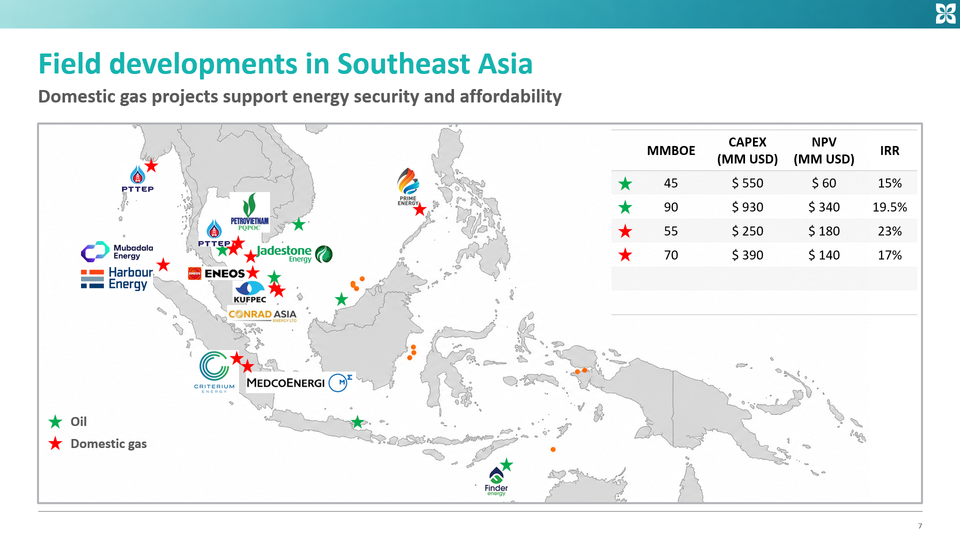

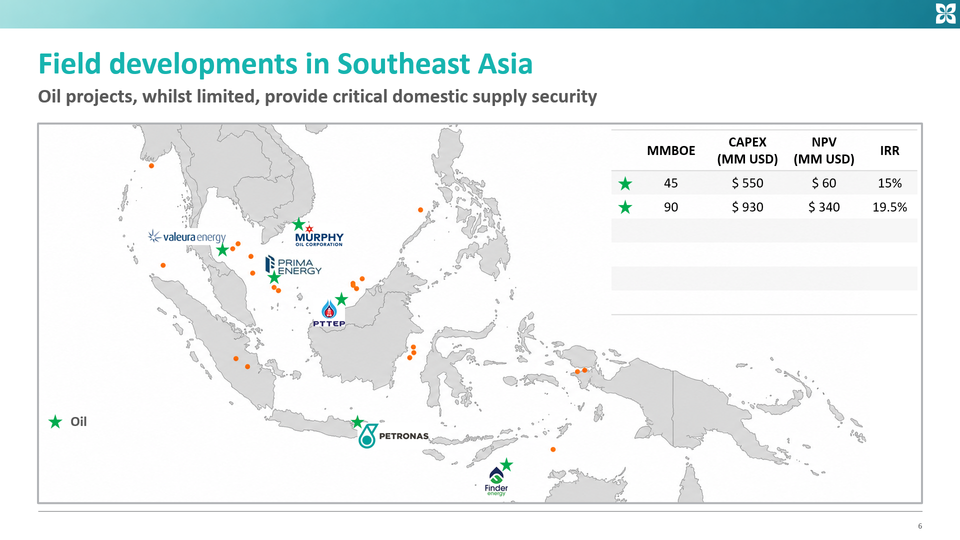

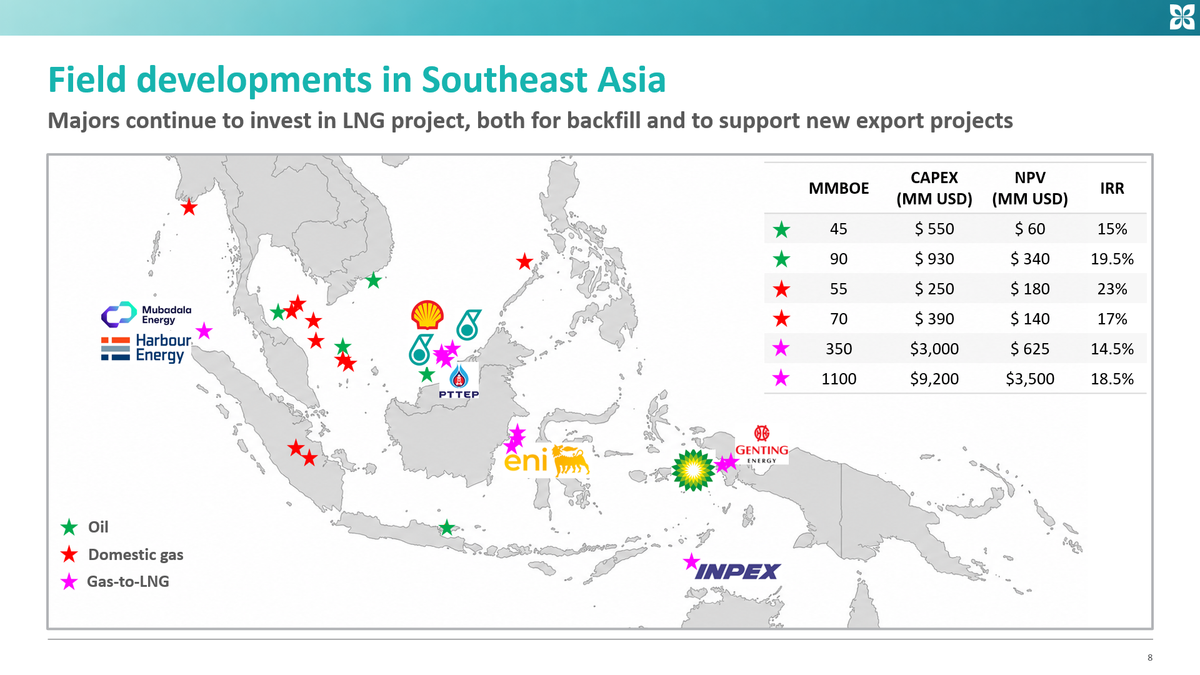

Gas-to-LNG developments in Southeast Asia

Kawi Energy presented at the SEAPEX / GESGB event in London on June 17th 2026. We were asked to talk about field developments in Southeast Asia.

We have split the presentation across a number of videos, with each video looking at a different resource class. In this third video, we look at a selection of gas-to-LNG projects, and what they tell us about the above-ground factors that can enable, or delay, development.

Gas-to-LNG is one of the most important upstream themes in Southeast Asia because it sits between domestic energy security and global gas markets. These developments can backfill existing LNG plants, support export revenues, monetise larger offshore resources and help preserve the role of established LNG hubs such as Bintulu, Brunei LNG, Bontang and Tangguh.

But gas-to-LNG is rarely simple. Projects need large resource bases, access to liquefaction, long-term buyers, competitive costs, partner alignment and government support. Increasingly, they also need credible carbon-management solutions, particularly where the gas contains high levels of CO₂, H₂S or other contaminants.

The strongest opportunities are therefore not simply the largest discoveries. They are the developments where upstream scale, LNG infrastructure, domestic supply obligations, carbon handling, buyers and political priorities can be aligned.

Rosmari-Marjoram, Malaysia

In Sarawak, Malaysia, Shell’s Rosmari-Marjoram development will bring new gas supply into the PETRONAS LNG Complex at Bintulu. The Rosmari and Marjoram deepwater sour gas fields were discovered in 2014 and lie around 220 km offshore Bintulu.

The main development challenge is the sour-gas composition, including high H2S content. The development plan combines offshore and onshore infrastructure: a deepwater subsea tie-back, an unmanned remotely operated wellhead platform, a 207 km sour wet-gas pipeline to shore, and an onshore gas plant at Bintulu to remove H2S from the gas before delivery into the LNG system.

The project is expected onstream towards the end of 2026 and is designed to deliver up to around 800 MMscf/d of gas.

Lang Lebah, Malaysia

Also in Sarawak, Malaysia, PTTEP’s Lang Lebah is one of the largest unsanctioned gas-to-LNG backfill opportunities in Southeast Asia. The field lies in Block SK410B in the Central Luconia gas province, around 90 km offshore Sarawak. PTTEP discovered Lang Lebah with the Lang Lebah-1RDR2 well in 2019 and confirmed the scale of the accumulation with the Lang Lebah-2 appraisal well, completed in January 2021. PTTEP described Lang Lebah-2 as its largest-ever gas discovery, while public company material estimates the field at around 5–6 Tcf of gas in place.

The development challenge is gas quality, with Lang Lebah containing high acid-gas contaminants, including CO₂ and H₂S. The development concept has centred on offshore production facilities, gas evacuation to Bintulu, and an onshore gas plant to treat the gas before delivery into the Malaysia LNG complex. The onshore plant FEED included CO₂ capture, compression and transport for offshore reinjection, with the Golok field reported as a potential sequestration site.

Lang Lebah is highly material, but it has not yet reached FID. The project has been delayed as PTTEP works to improve the economics, with industry reporting pointing to EPC bids coming in significantly above budget and gas-commercialisation issues still needing resolution. PTTEP is now understood to be re-engineering the development to optimise costs, and one possible route forward is a more integrated sour-gas development concept that could share infrastructure with other challenging Sarawak fields and reduce unit costs.

Kasawari, Malaysia

Continuing in Sarawak, PETRONAS’ Kasawari field is already producing gas into the Bintulu system. The field lies in Block SK316, around 200 km offshore Sarawak, and was discovered in 2011. It contains approximately 10 Tcf of natural gas resources and is designed for a gas sales rate of around 545 MMscf/d. First gas was achieved in August 2024 at an initial rate of around 200 MMscf/d, with supply intended for the PETRONAS LNG Complex at Bintulu as well as domestic gas demand.

The upstream development is built around a conventional offshore production system, with field facilities including a central processing platform, a flare platform and a wellhead platform, interconnected by bridges. Gas is exported through an 81 km pipeline to a new riser platform at the E11 production hub for onward delivery to Bintulu.

The remaining major development element is CO₂ management. Kasawari has a high CO₂ content, and the CCS project is designed to separate CO₂ from the produced gas, compress it, transport it through a dedicated subsea pipeline, and inject it into the depleted M1 field. Public project descriptions have cited around 71–76 million tonnes of CO₂ storage over the project life, with annual capture of around 3.3 Mtpa. PETRONAS is now reported to be targeting first CO₂ injection as early as 2027.

Kelidang Cluster, Brunei

In Brunei, PETRONAS’ Kelidang Cluster is a newly sanctioned gas-to-LNG backfill project for the Brunei LNG system. The development sits in offshore Block CA2 and covers ultra-deepwater gas discoveries made in 2013 and 2015.

FID was taken on November 7, 2025 and the project is targeting commercial production around 2030, with planned natural gas output of around 390 MMscf/d during the stable production phase. The gas is expected to be supplied to Brunei LNG and exported as LNG to customers in Japan and other Asian markets.

The development plan is based on a new floating production unit, a subsea production system and a gas export pipeline to Brunei LNG. The FPU is designed with gas processing capacity of around 450 MMscf/d and condensate handling capacity of around 1,170 b/d.

Eni / PETRONAS Kutei Basin projects, Indonesia

In Indonesia, Eni has moved quickly to sanction a new wave of deepwater gas-to-LNG backfill projects in the Kutei Basin offshore East Kalimantan. In March 2026, Eni took FID on two linked developments: the Gendalo and Gandang project, and the Geng North and Gehem project, or Northern Hub. Together, the four fields contain nearly 10 Tcf of gas initially in place and around 550 million barrels of associated condensate.

The Gendalo and Gandang development will backfill the existing Jangkrik production hub, while the Northern Hub will be developed around a new FPSO with capacity to process more than 1 Bscf/d of gas and 90,000 b/d of condensate. Production from the projects is expected to start in 2028, with plateau targeted in 2029. Gas from the new hubs will be transported onshore through an export pipeline to a receiving facility that supplies both Indonesia’s domestic gas network and the Bontang LNG plant. Eni has also said the development plan includes extending the operating life of Bontang LNG by reactivating one currently idle liquefaction train, Train F.

Eni has also added further running room in the basin through the Geliga discovery, announced in April 2026. Preliminary estimates put Geliga at around 5 Tcf of gas in place and 300 million barrels of condensate, and well testing has indicated strong deliverability. Eni has described the discovery as potentially supporting a further production hub, reinforcing the idea that the Kutei Basin is becoming a multi-hub gas province tied into both domestic gas infrastructure and Bontang LNG.

These Kutei Basin assets also sit within the broader SEARAH platform established by Eni and PETRONAS. The 50:50 joint venture combines 19 gas-producing and development assets across Indonesia and Malaysia and is intended to support a large regional investment programme.

South Andaman, Indonesia

In Indonesia’s Andaman Sea, Mubadala Energy’s Layaran and Tangkulo discoveries raise the possibility of a new gas province offshore North Sumatra, with potential LNG-linked monetisation over time. Mubadala announced Layaran-1 in South Andaman in December 2023, with potential for more than 6 Tcf of gas-in-place. It followed this with Tangkulo-1 in May 2024, with potential for more than 2 Tcf of gas-in-place.

For now, the clearest commercial route is domestic gas. In December 2025, Mubadala Energy and PLN Energi Primer Indonesia signed a Heads of Agreement covering potential gas supply from the Andaman Sea, with an emphasis on North Sumatra and Aceh. However, given the potential scale of the resource, the partners will also be looking at LNG-linked monetisation options, be this FLNG or an onshore LNG plant. The challenge will be aligning that basin-scale opportunity with Indonesia’s domestic energy-security and regional-development priorities. That tension is already visible, with Aceh’s provincial government pushing for onshore processing and downstream development to capture more local economic benefit.

The ownership structure may also evolve as the development matures. Harbour has been reshaping its Southeast Asia portfolio, and is currently running a process to divest its Andaman interests. Regardless of this process, Mubadala may still look to bring in a partner with deeper LNG development, marketing or balance-sheet capacity.

Abadi LNG, Indonesia

In Indonesia, INPEX’s Abadi LNG project in the Masela Block is one of Asia’s largest undeveloped gas-to-LNG projects. The Abadi gas field was discovered in 2000, but the project has taken more than two decades to move toward sanction. The current development concept is an onshore LNG scheme designed to produce around 9.5 mtpa of LNG, up to 35,000 b/d of condensate and around 150 MMscf/d of pipeline gas.

Abadi is also the clearest example in the region of how large gas-to-LNG projects can become politically and commercially heavy. The project was delayed for years, including a major redesign from an FLNG concept to an onshore LNG development, and the revised development plan now includes CCS. Indonesia approved the revised plan of development in December 2023, FEED started in August 2025, and Reuters reported in February 2026 that INPEX planned to start EPC tendering in mid-2026, with Indonesian authorities working to remove permitting and local-content hurdles.

Recent progress is real. In May 2026, INPEX announced agreements in principle with potential LNG and pipeline gas buyers, including BP, PGN, PLN Energi Primer Indonesia and Shell Eastern Trading. That gives the project clearer commercial momentum after years of delay, although FID has still not been taken.

Abadi is the warning label for South Andaman. Large resources can support LNG, domestic gas, pipeline supply and regional industrial benefits, but the more strategic the project becomes, the more political and complex it gets. For South Andaman, the lesson is that LNG optionality may increase the value of a large gas resource, but it also raises the burden of aligning upstream economics, domestic supply obligations, onshore development expectations, permitting, CCS and buyer commitments.

Tangguh UCC, Indonesia

The Tangguh LNG plant has been producing LNG since 2009. The current story is about sustaining and extending gas supply through the Ubadari, CCUS and Compression project, usually referred to as Tangguh UCC. The US$7 billion project reached FID in November 2024 and comprises the Ubadari gas field development, enhanced gas recovery through CCUS at the Vorwata field, and new onshore compression. Production and operations are expected to start in stages from 2028, and the project is intended to unlock around 3 Tcf of additional gas for the Tangguh LNG system.

The CCUS element is central to the UCC project. The scheme separates reservoir CO₂ from produced gas and reinjects it into the Vorwata field, both to sequester CO₂ and support enhanced gas recovery. bp describes Tangguh CCUS as Indonesia’s first CCUS project developed at scale, with potential to sequester around 15 million tonnes of CO₂ in its initial phase.

The challenge for the UCC project is more technical and execution-related: integrating Ubadari, CCUS and compression into a producing LNG system while maintaining reliable supply from one of Indonesia’s core LNG export assets.

Genting / Kasuri FLNG, Indonesia

Genting’s Kasuri PSC in West Papua combines upstream gas, a dedicated FLNG facility and domestic industrial use. The revised POD for the Asap, Merah and Kido structures uses 2.674 Tcf of gas-in-place and allocates supply to two markets: 230 MMscf/d to an FLNG facility for 18 years, and 101 MMscf/d to an ammonia and urea plant in West Papua for 17 years.

The FLNG project is expected to have capacity of around 1.2 mtpa. Genting signed a US$962.8 million contract with Wison New Energies for the facility, which will receive feedgas from the Asap, Merah and Kido structures in the Kasuri block.

Conclusions

Taken together, these projects illustrate how the gas-to-LNG story in Southeast Asia now spans a diverse set of opportunities and development models. In many cases, the LNG plants already exist; the challenge is securing enough competitive upstream gas to keep them full. At the same time, new greenfield LNG projects are still being developed and discussed, particularly where the resource base is large enough to support a broader basin-scale development.

For backfill projects, the liquefaction plants, export markets and operating expertise already exist. The value lies in developing new upstream resources quickly enough to sustain those LNG systems, while integrating carbon management, domestic gas obligations and regional industrial development into the same project.

For greenfield projects, the challenge is broader. Large discoveries can create the scale needed for LNG, but they also become more strategic for host governments. Domestic gas supply, power generation, industrial development, local employment, onshore infrastructure and regional economic benefits all become part of the development debate. That can strengthen the political case for a project, but it can also make the commercial model harder to align.

The result is that success is no longer determined by resource size alone. The projects most likely to move forward are those that can align upstream scale, liquefaction access, carbon management, commercial competitiveness, partner capability and government priorities. As the projects in this review demonstrate, that alignment has become the defining challenge — and the defining opportunity — for Southeast Asia’s next generation of gas development.