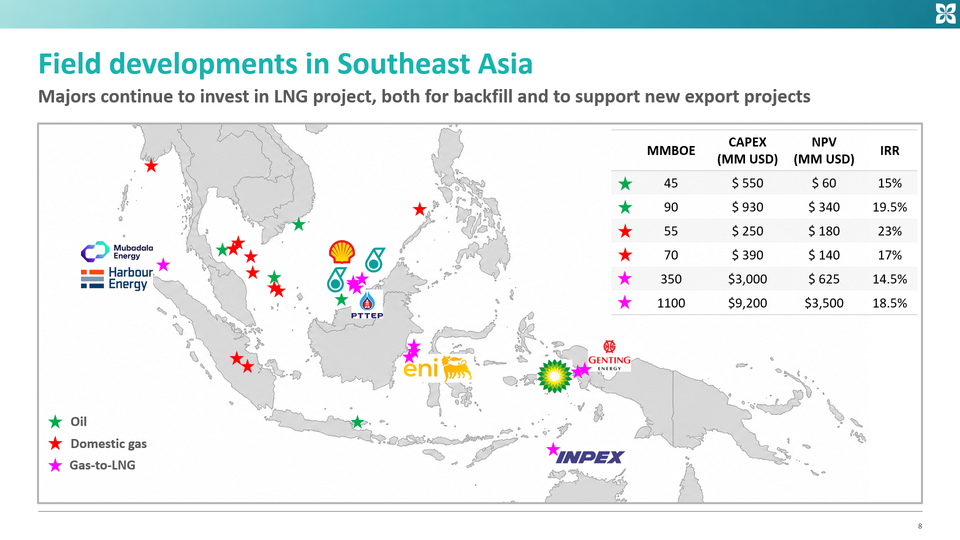

Oil field developments in Southeast Asia

Kawi Energy presented at the SEAPEX / GESGB event in London on June 17th 2026. We were asked to talk about field developments in Southeast Asia.

We have split the presentation across a number of videos, with each video looking at a different resource class. In this first video, we look at a selection of oil projects, and what they tell us about the above-ground factors that can enable, or delay, development.

Whilst Southeast Asia is gas-weighted, oil discoveries are often simpler to monetise. Crude can be stored, lifted, blended and sold into regional or global markets, without the need for a dedicated power plant, domestic gas buyer or long-term gas sales agreement.

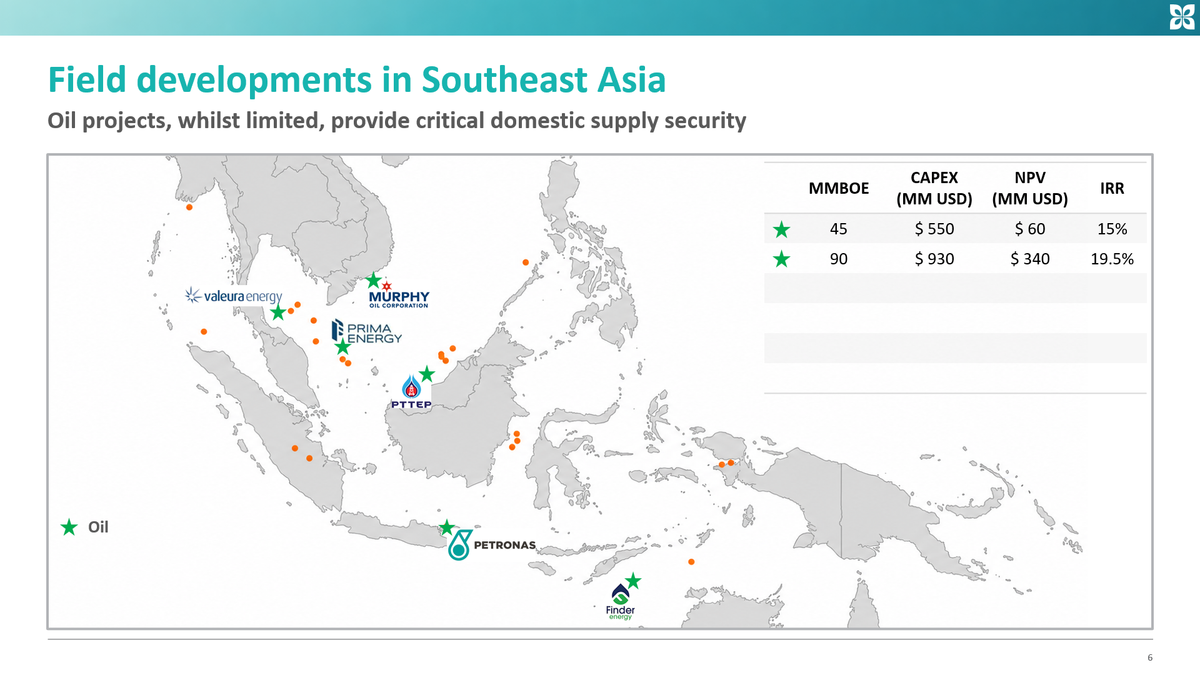

Vietnam - Murphy - Lac Da Vang / Hai Su Vang

Murphy’s Lac Da Vang (LDV) oil field development is located offshore Vietnam in the Cuu Long Basin, approximately 120 km east of Vung Tau. The project is operated by Murphy, with partners PVEP and SK Earthon.

The LDV field was discovered in 2010 and FID was taken in 2023. The field is expected to come onstream in late 2026. The development is centred on the LDV-A processing platform, supported by an FSO, with development drilling and follow-on work continuing through the end of the decade. According to Murphy’s latest guidance, estimated gross recoverable resources are around 100 MMBOE, with expected gross peak production of approximately 25–37.5 MBOE/d.

Murphy has also made further nearby discoveries in Block 15-1/05, including Lac Da Trang (LDT, 2019) and Lac Da Hong (LDH, 2025), alongside the earlier Lac Da Nau (LDN, 2009) discovery. The LDT discovery has been incorporated into the LDV development phase, while LDH and LDN could potentially be developed as future tie-backs.

In neighbouring Block 15-2/17, Murphy discovered Hai Su Vang (HSV) in 2025. This appears to be a potentially larger discovery and, subject to continued appraisal success, could support a separate development hub or form part of a broader Murphy-led Cuu Long Basin oil growth platform.

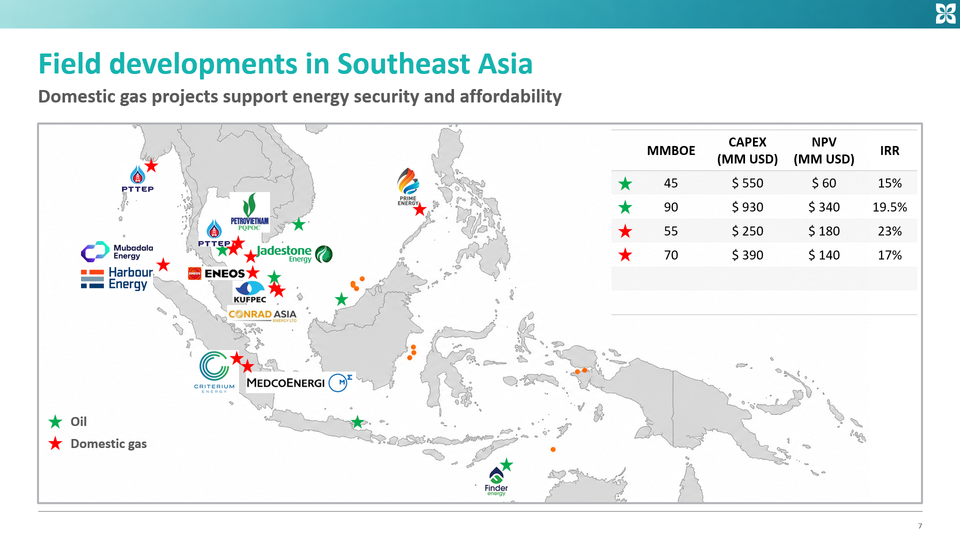

Indonesia - PETRONAS - Hidayah

PETRONAS’ Hidayah oil field development is located offshore East Java, Indonesia, in the North Madura II PSC, approximately 6–7 km north of Madura Island. The field lies in shallow water of around 25 m and is operated by PETRONAS, although the asset will likely form part of PETRONAS and Eni’s SEARAH joint venture.

The Hidayah field was discovered in 2021. The Plan of Development was approved in 2023, with FID reached in late 2024 and announced by PETRONAS in January 2025. The field is expected to come onstream in 2027.

The Phase 1 development is centred on an integrated wellhead and central processing platform, supported by a leased spread-moored FSO. The initial development scope includes four oil production wells, a rigid oil pipeline from the platform to a pipeline end termination, and a flexible riser connection to the FSO. According to SKK Migas guidance at the time of POD approval, Hidayah holds around 88.55 MMstb of oil reserves, with initial production expected at around 9,000 bopd and peak production of around 25,000 bopd later in the field life.

Hidayah is an important near-term oil development for PETRONAS in Indonesia and supports the company’s broader East Java growth strategy. PETRONAS also operates several nearby PSCs offshore East Java, including Ketapang, North Ketapang and Serpang. In 2026, PETRONAS announced the Barokah-1 hydrocarbon discovery in the neighbouring North Ketapang PSC, which reinforces the exploration potential of the Northern Madura region.

Malaysia - PTTEP - Sirung / Chenda

PTTEP’s Sirung and Chenda development is located offshore Sarawak, Malaysia, in Block SK405B, within the Balingian Province of the Sarawak Basin. The project is operated by PTTEP, with partners PETRONAS Carigali and Mitsui Energy Development.

The Sirung field was discovered in 2021, followed by the Chenda discovery in 2023. FID for the development of the two fields was reached in February 2026, marking PTTEP’s first greenfield development sanction in Malaysia. The development concept comprises a central processing platform and a wellhead platform, with first oil targeted during 2028. PTTEP has indicated combined production capacity of approximately 15,000 bpd.

Sirung and Chenda are important for PTTEP because they move its Malaysian portfolio from exploration success into operated greenfield development. The project also supports PTTEP’s broader Sarawak growth strategy.

Thailand - Valeura - Wassana redevelopment

Valeura’s Wassana redevelopment is located offshore Thailand in the Gulf of Thailand, within Licence G10/48, where Valeura holds a 100% operated interest.

The field is already producing, but current production is constrained by the existing MOPU infrastructure, which is expected to reach end of life by the end of 2027. Valeura took FID on the Wassana redevelopment in May 2025. The project is based on replacing the existing MOPU with a new-build central processing platform (CPP), designed to optimise recovery from the wider G10/48 licence and extend the field’s economic life. The new CPP will have 24 production well slots and is expected to be installed and ready for development drilling by late 2026. First oil from the new facilities is expected in Q2 2027, with production expected to increase to around 10,000 bpd in the second half of 2027.

The redevelopment is expected to materially increase the value and life of the field. Valeura estimates that Wassana 2P reserves increase to 20.5 MMbbl, around 18 MMbbl higher than under a no-further-action case using the existing infrastructure only. The project also extends the end-of-field life by around 16 years to 2043. Facilities capex is estimated at approximately US$120 million, mostly across 2025–2026, and the project is expected to be fully funded from Valeura’s balance sheet.

The initial drilling programme is expected to comprise 16 horizontal development wells and one water injection well. The new CPP has also been designed to support future “hub-and-spoke” growth, with potential tie-backs of satellite oil accumulations to the north and south of Wassana, including the Nirami and Mayura areas. This makes Wassana an important redevelopment for Valeura, both as a near-term production growth project and as a potential hub for further commercialisation of resources across Licence G10/48.

Timor-Leste - Finder - Kuda Tasi / Jahal

Finder’s Kuda Tasi / Jahal oil field development is located offshore Timor-Leste in PSC TL-SO-T-19-11, within the Laminaria High oil province. The project is operated by Finder, with TIMOR GAP as its joint venture partner.

The Jahal field was discovered in 1996 and the Kuda Tasi field in 2001. Finder assumed operatorship of PSC 19-11 in 2024 and has since moved the project rapidly toward development. In March 2026, Timor-Leste’s Autoridade Nacional do Petróleo approved the Kuda Tasi and Jahal development area, following Finder’s declaration of commerciality. Finder and TIMOR GAP subsequently submitted the Field Development Plan in May 2026, with FID expected to follow once regulatory approval is received.

The selected development concept is based on three production wells connected via an electrical submersible pump manifold to the Petrojarl 1 FPSO through flexible flowlines. Finder has highlighted the potential for initial production of around 25,000–40,000 bopd, depending on facility configuration, although the development is expected to be relatively short-cycle with high early production followed by decline. Current planning points to FID in 2026 and first oil in late 2027 or early 2028.

The KTJ project is important for Finder because it would transform the company from an explorer into an offshore oil producer. It is also strategically important for Timor-Leste, as it is expected to be the country’s next offshore oil development and could provide a hub for future tie-backs of nearby discoveries and prospects, including Krill and Squilla.

Indonesia - Prima Energy - Ande Ande Lumut

Prima Energy’s Ande Ande Lumut (AAL) oil field development is located offshore Indonesia in the Northwest Natuna PSC, in the West Natuna Sea. The field lies in shallow water of around 70–76 m, approximately 260 km north-northwest of Matak in the Anambas Islands. The Northwest Natuna PSC is operated by Prima Energy.

The AAL field was discovered in 2000, with appraisal wells drilled in 2006 and 2016. The field contains heavy oil in unconsolidated sand reservoirs, with reported test rates of 1,220 bopd of 15° API oil from the K sand and 800 bopd of 12° API oil from the G sand. Prima’s published materials indicate oil in place of around 214 MMstb in the K and G2 sands, with expected recovery of around 42.7 MMstb.

The field had previously been approved for development, but the current project is based on a revised Plan of Development approved in March 2024. The revised concept uses a central production platform / wellhead central processing platform and a leased spread-moored FSO, replacing earlier concepts and aiming to commercialise the field using horizontal wells, sand control, inflow control devices and electrical submersible pumps. Prima says the development will require at least 20 production wells, with the first phase expected to include seven horizontal production wells targeting the Oligocene Upper Gabus G and K sand layers.

The initial facilities scope includes a CPP / WH-CPP designed to process around 20,000 bopd of heavy oil and 100,000 bwpd, connected to a leased FSO with around 600,000 barrels of crude storage capacity. Prima’s project page indicates CPP construction is expected to start in 2026, with first oil targeted in late 2027 / 2028.

AAL is important for Prima Energy because it is the company’s flagship offshore oil development. It is also strategically relevant for Indonesia, as SKK Migas has highlighted the project’s potential contribution to national oil production and energy security.

The project remains execution-sensitive, given the heavy-oil reservoir, unconsolidated sands, high water-handling requirement and reliance on successful horizontal well delivery, but the approved revised POD and ongoing contracting activity indicate that the redevelopment has moved into a more active development phase.

Conclusion

The recent wave of Southeast Asian oil developments shows that the region’s upstream story is not only about gas. Modest-sized offshore oil accumulations can still attract capital where the development concept is simple, infrastructure is available or scalable, and fiscal terms allow operators to move quickly.

A key attraction is speed to market. Some projects are moving from discovery to sanction or first oil on relatively short timelines, while others are reviving older discovered resources through simpler facilities, phased drilling and floating storage. In both cases, oil offers a clearer route from resource to cash flow than many gas projects, which can depend on domestic demand, pipeline access, LNG capacity or long-term offtake negotiations.

The opportunity is real, but selective. The strongest projects combine discovered oil, shallow-water settings, low-complexity facilities and follow-on resource potential. Risks remain around cost inflation, drilling performance, reservoir deliverability and regulatory timing, but Southeast Asia’s next phase of upstream growth could still include a meaningful number of pragmatic, oil-led developments.